A profit and loss report, also known as an “income statement” summarises business profitability over a specific period of time. Commonly used to show business performance on a monthly, quarterly, or annual basis.

A profit and loss report shows the total income and total expenses of a business for monitoring business activities. For business owners, it highlights the strengths and weaknesses of the business and for investors, it is a gauge of the financial health of a potential investment.

The profit and loss report is one of three core financial statements (balance sheet and statement of cash flows, being the other two) that are used to evaluate a business’s financial performance, position, and value.

The profit and loss report consists of two sections:

- Revenue – details of all income from your primary business activities (e.g. sale of products and/or services), any revenue from any investment activities (e.g. dividend and/or bank interest), and any other financial gains (e.g. sale of assets and/or other investments)

- Expenses — details of all expenditures related to the primary business activities (e.g. material and labour costs), any secondary expenditure, and any other losses during the period.

Revenue details the sales of products and services, which is the most important part of business activity. Other revenue is important, but not as relevant as the main sales of the business.

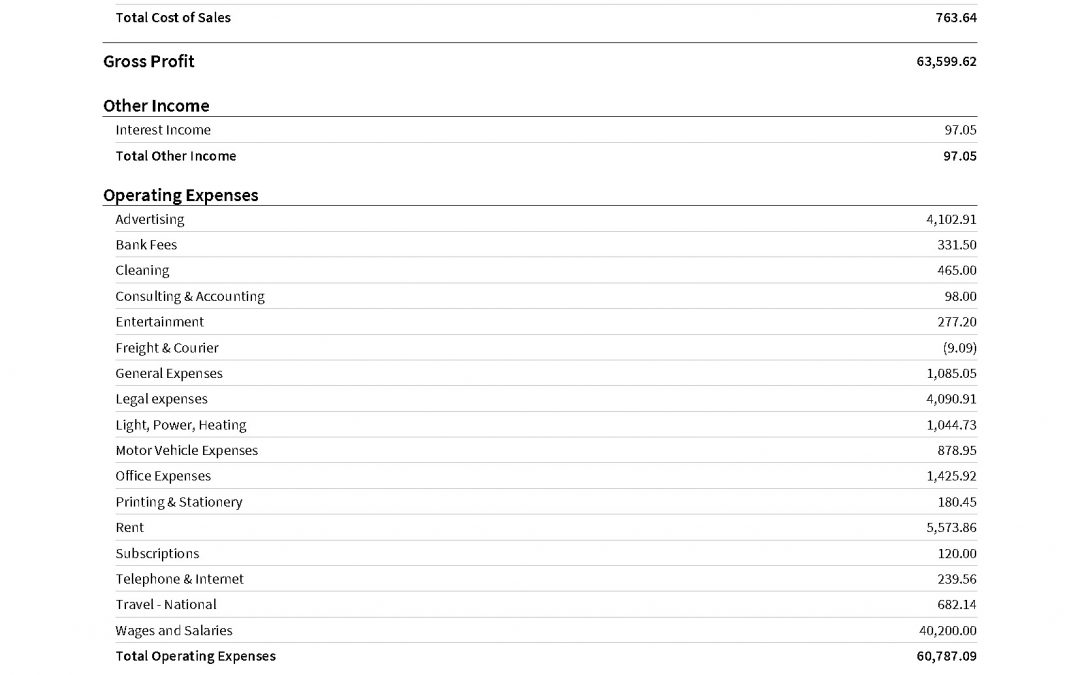

Expenses are divided into two parts; the cost of goods sold and operating expenses.

- Cost of goods sold are the expenses that directly relate to the production and labour of the good and services sold (e.g. cost of raw materials and direct labour costs)

- Operating expenses are expenses not directly related to the production and labour of the goods and services sold (e.g. administration costs, utilities, marketing, licensing, etc.)

Costs of goods sold increase and decrease based on the volume of sales, where operating costs tend to be separate from the direct effects of sales.

Profits are calculated using the below formulas:

Revenue – Costs of Sale = Gross Profit

(the difference between total sales and the cost of producing the goods and services sold)

Gross Profit / Revenue = Gross Profit Margin

(shows what proportion of gross profit is kept from each dollar of revenue generated

e.g. 25% gross profit margin means $0.25 of profit is kept from every $1.00 of revenue generated)

Gross Profit – Operating Expenses = Operating Profit

(profits generated from core business operations, excluding interest and taxes)

Operating Profit – Taxes – Interest = Net Profit

(also known as the “bottom line” – net profit is the amount earned or lost after paying all expenses)